Thankfully, the incidence of COVID-19 in Uganda is very low in comparison to other countries—the country has so far recorded 260 cases, with 63 recoveries, and no COVID-19 related deaths as of this writing. Indeed, early on, Uganda adopted a number of containment measures to curb the spread of the virus, including the closure of schools, restrictions on internal and international travel, use of hand sanitizer, improved handwashing stations, social distancing, and even lockdown, among others. While these measures may have contributed to the successful reining in of the virus, those same restrictions have hit business operations hard.

A recent rapid survey of businesses by the Economic Policy Research Centre (EPRC) in Uganda reveals that three-quarters of the surveyed businesses have laid off employees due to the risks presented by COVID-19 and subsequent containment measures. Indeed, the results suggest that lockdown measures have reduced business activity by more than half. In terms of sectors, we find that businesses in agriculture have experienced the largest constraints in access to both inputs and markets for outputs due to control measures such as transport restrictions, quarantine, social distancing, and bans on weekly markets.

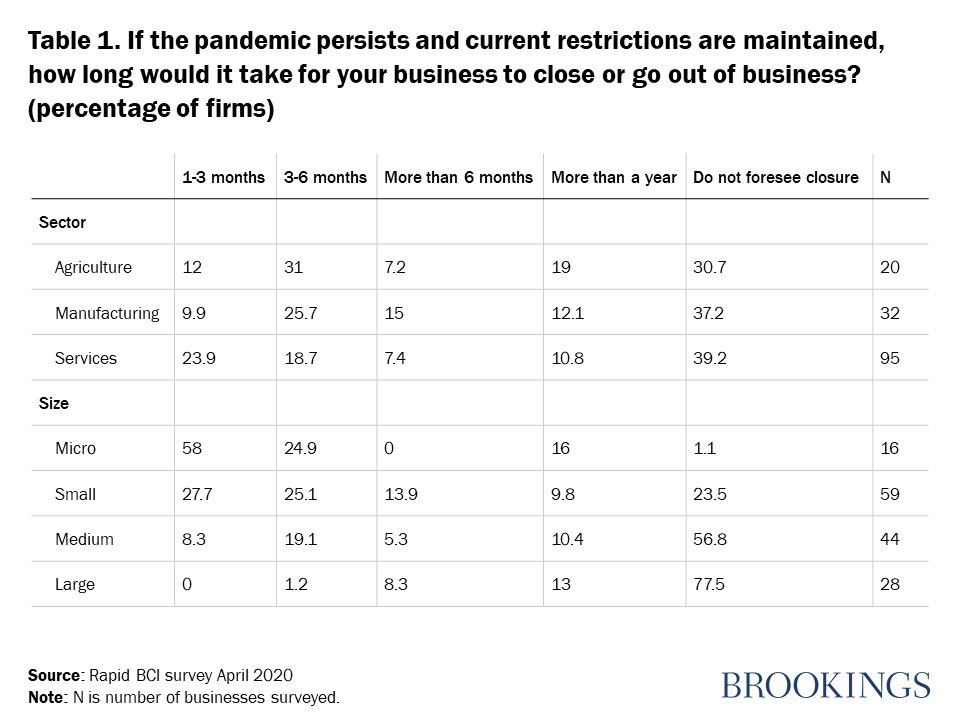

In short, we find that micro and small businesses experienced a larger decline in businesses activity compared to medium and large firms—an unsurprising finding since most of the country’s micro and small businesses halted operations due to their inability to implement preventative health measures such as provision of on-site lodging for employees, and sanitizers and handwashing equipment for customers. These preventive measures have resulted in an increase in operating expenses for businesses that continued to stay open. Consequently, a majority of micro and small businesses, particularly in the service sector, predict they will have to close within one to three months if the pandemic persists and current restrictions are maintained (Table 1). On the other hand, the majority of the medium and large firms do not foresee closure. Sectoral analysis reveals slightly higher resilience among agriculture and manufacturing firms compared to service sector firms.

Unemployment in agriculture already high; service sector expected to follow suit in 6 months

The survey results reveal that the workforce in Ugandan agricultural businesses has undergone the largest restructuring. About 80 percent of businesses in the agriculture sector have reduced their workforce by more than a quarter. Results indicate that a severe decline in agricultural demand may be to blame: Close to 71 percent of surveyed businesses in agriculture reported severe decline in demand compared to 47 percent in manufacturing and 49 percent in services. At the same time, a significantly high percentage of manufacturing businesses have laid off employees, with 41 percent of them reducing employees by more than one half.

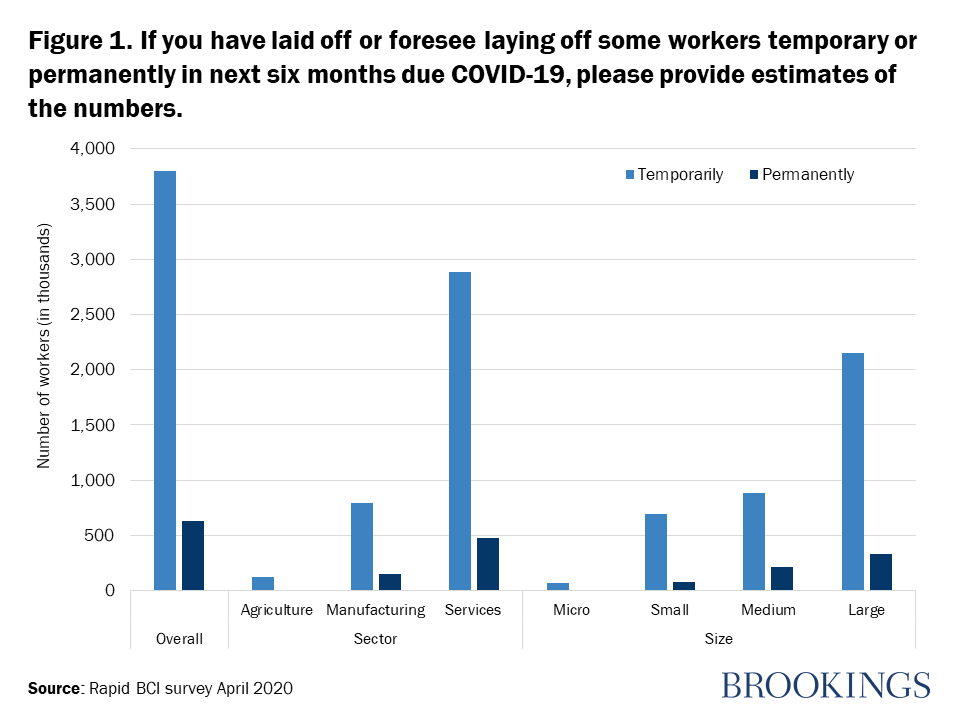

Unemployment will likely worsen if the risks associated with COVID-19 persist and containment measures are sustained or escalated. Surveyed businesses indicated they would lay off a total of 1,662 workers temporarily and 406 permanently if the threat of COVID-19 and associated containment measures persist for the next six months. Applying sample weights obtained from the Uganda Bureau of Statistics on these numbers, we estimate that 3.8 million workers will lose their jobs temporarily while 625,957 risk losing their employment permanently if the threat of COVID-19 and associated containment measures persist for the next six months (Figure 1). Such layoffs would constitute a reduction of 42 percent in temporary employment and 7 percent in permanent employment. Notably, over 75 percent of employees projected to lose their jobs permanently are from the service sector. Given most services in Uganda involve face-to-face interaction that contravenes the social distancing requirement, this finding is not surprising.

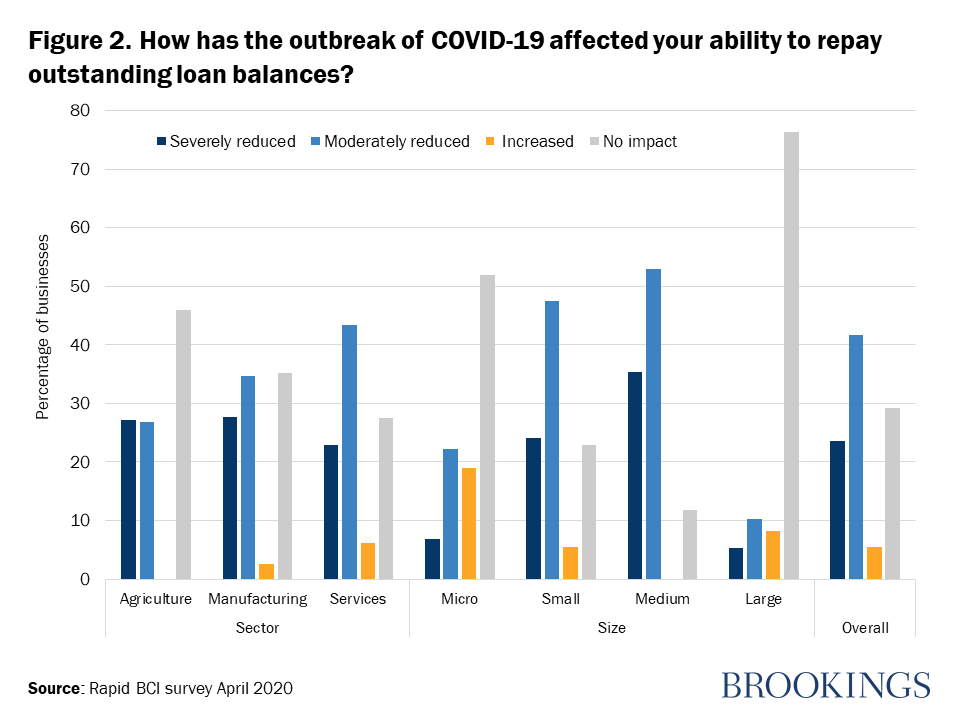

In addition to the lower demand and higher costs of safety measures, responding businesses shared other worrying concerns, including lessened production and productivity, reduced supply of inputs, and credit and liquidity constraints. Indeed, risks associated with COVID-19 have exacerbated preexisting credit and liquidity constraints among micro, small, and medium enterprises (MSMEs). Indeed, 69 percent of businesses surveyed reported a decline in access to credit, with 34 percent experiencing severe decline (a more than 50 percent decline in credit) (Figure 2).

Notably, a relatively high percentage of small and medium businesses in the services sector in particular reported a decline in access to credit and financial liquidity compared to large businesses. This trend may be because lending institutions already consider them highly risky, and those businesses are more likely to become insolvent if COVID-19 persists and restrictions are maintained. On a sectoral level, high percentages of businesses in manufacturing and services reported a decline in ability to repay outstanding debts due to the outbreak of COVID-19 compared to those in agriculture. This finding might suggest that fewer businesses in agriculture qualify for credit. Even for those with loans, the amounts are relatively small—a sign of how poorly agriculture is resourced as far as access to credit is concerned.

Our analysis also shows that the majority of small and medium businesses, particularly in manufacturing, have experienced a severe decline in access to inputs, alluding to the risk of overreliance on international rather than regional or domestic supply chains for raw materials and intermediates. This finding calls for firms, especially MSMEs, to explore the possibility of regional or domestic value and supply chains to stabilize their sources of inputs, while also saving on scarce foreign exchange.

Recommended actions

From the survey, we see that micro, small, and medium enterprises in Uganda are getting the squeeze in the face of COVID-19 and associated business restrictions. From the analysis, we recommend that the authorities offer liquidity interventions to support firms in addressing immediate liquidity challenges, reduce layoffs, and avoid firm closures and bankruptcies. In order to free up more cash for businesses, the government may also consider the following: (i) tax rate reduction, (ii) reducing taxable income, (iii) offering tax credits, and (iv) offering tax refunds. In addition, the government should pay all the outstanding arrears against supplies made to government.

Commercial banks should consider proactively providing emergency loans to MSMEs with flexibility in repayments. The government could recapitalize commercial banks and micro-financial institutions by extending cash loans or by loosening the liquidity reserve requirements to provide financial institutions with the extra liquidity required to provide flexible emergency loans. The above efforts could be complemented by extension and diversification of partial credit guarantee schemes for loans provided by private banks. Alternatively, the government could offer concessional loans through the Uganda Development Bank. In this vein, the government of Uganda has already sought and received a $500 million loan from the International Monetary Fund. The government is also seeking debt repayment rescheduling, which would free up to $2 billion for such purposes.

Use of technology for access to credit should also be escalated during this crisis. For example, mobile money and other e-platforms can simplify loan application processes and reduce turnaround times of MSME loans.

Finally, the Credit Reporting Bureau should be on the lookout for unintended defaults. In this case, all financial institutions should continue to share credit information with regulators. Finally, the government should consider amending the legal framework on bankruptcy with temporary measures to prevent liquidation.

This blog was first published on the Brookings Website. Access the original post here.